Wall Street Predicts Major Home Price Drop Since Great Depression

Wall street expects second biggest home price drop since great depression – Wall Street predicts the second biggest home price drop since the Great Depression, sending shockwaves through the housing market and raising concerns about the broader economy. This prediction, fueled by rising interest rates, inflation, and affordability issues, paints a grim picture for both homeowners and potential buyers.

The potential impact of this price drop is significant. Experts warn of a ripple effect, impacting mortgage lenders, investors, and the real estate industry as a whole. With a downturn of this magnitude, economic growth and stability could be at risk.

The Magnitude of the Expected Home Price Drop

Wall Street’s prediction of the second biggest home price drop since the Great Depression is a serious warning signal for the housing market and the broader economy. This forecast signifies a potential for a significant decline in home values, raising concerns about the financial well-being of homeowners and the overall stability of the housing market.

The Significance of the Second Biggest Drop

The comparison to the Great Depression highlights the potential severity of the anticipated price drop. The Great Depression saw a catastrophic decline in home values, contributing to widespread economic hardship and instability. While the current situation is not expected to reach the same level of devastation, the magnitude of the predicted drop underscores the potential for substantial financial losses for homeowners and ripple effects across the economy.

Comparing the Current Situation to the Great Depression

While the current economic environment is different from the Great Depression, there are some key similarities that contribute to the current housing market concerns. Both periods witnessed significant economic downturns, leading to a decrease in demand for housing and a subsequent decline in prices. In the current situation, factors such as rising interest rates, inflation, and potential recessionary pressures are contributing to a decrease in affordability and a slowdown in home sales.

The Potential Impact of the Drop on Homeowners and the Economy

A significant drop in home prices could have several negative consequences for homeowners and the broader economy.

Impact on Homeowners

- Negative Equity: Homeowners who bought at peak prices could find themselves in negative equity, meaning their mortgage debt exceeds the value of their home. This can make it difficult to sell or refinance, trapping homeowners in their properties.

- Reduced Wealth: A drop in home prices reduces the value of homeowners’ primary asset, impacting their net worth and potentially leading to financial hardship.

- Increased Foreclosures: A decline in home values can lead to an increase in foreclosures as homeowners struggle to make their mortgage payments.

Impact on the Economy

- Reduced Consumer Spending: Homeowners facing financial difficulties may reduce their spending, contributing to a slowdown in economic growth.

- Impact on the Construction Industry: A decline in home sales can negatively impact the construction industry, leading to job losses and reduced investment.

- Financial Market Instability: A sharp drop in home prices could lead to instability in the financial markets, as banks and other financial institutions face losses on mortgage-backed securities.

Factors Contributing to the Price Drop

The anticipated decline in home prices is a complex phenomenon driven by several interconnected economic factors. Understanding these factors is crucial for navigating the current housing market and making informed decisions.

Rising Interest Rates

The Federal Reserve has been aggressively raising interest rates in an effort to combat inflation. This has directly impacted the housing market by making mortgages more expensive. Higher interest rates translate into higher monthly mortgage payments, reducing affordability for potential homebuyers. For example, a 30-year fixed-rate mortgage with a 5% interest rate would require a significantly higher monthly payment than a similar mortgage with a 3% interest rate.

The news that Wall Street expects the second biggest home price drop since the Great Depression is certainly concerning. But while the economy may be taking a downturn, the political landscape is heating up with the news that a federal judge has unsealed more portions of the Trump search warrant affidavit here. It seems like the news cycle is dominated by these major shifts, and it’s hard to know what to expect next for both our wallets and our political future.

This has led to a slowdown in demand, as buyers become more hesitant to commit to large monthly expenses.

Inflation and Affordability

Inflation has been a significant factor contributing to the housing market slowdown. Rising prices for essential goods and services have eroded purchasing power, making it more challenging for households to afford a home. For instance, a 10% increase in inflation can significantly reduce a buyer’s ability to qualify for a mortgage, as lenders typically assess affordability based on income and expenses.

The news of Wall Street predicting the second largest home price drop since the Great Depression is certainly concerning. It’s hard to ignore the parallels between the economic anxieties of the past and the current climate. But while we’re grappling with potential financial turmoil, it’s worth remembering that the legal landscape is also filled with its own dramas. For instance, the recent ruling preventing John Durham from discussing the alleged links between the Trump dossier sources and Russian intelligence at trial, as reported in this article , adds another layer of complexity to the political scene.

It’s a reminder that even as we navigate the economic storm, there are other crucial battles being fought in the courtroom, with potential ramifications for our future.

This has put downward pressure on home prices as buyers become more price-sensitive and seek out more affordable options.

Wall Street is predicting a second major home price drop, rivaling the Great Depression, and it’s hard to ignore the potential impact of our national debt, which recently hit a record-breaking $31 trillion. This staggering figure, as reported in this article , is a direct result of the Biden administration’s spending spree, and it could certainly contribute to the economic instability that’s fueling this predicted housing market downturn.

Economic Uncertainty

The current economic climate is characterized by uncertainty, which is affecting consumer confidence and spending. Concerns about a potential recession, job losses, and the overall economic outlook have made potential homebuyers more cautious. In such an environment, people tend to postpone major purchases, including buying a home, until they feel more secure about their financial situation.

Potential Consequences of the Price Drop

A significant decline in home prices could have far-reaching consequences, affecting not only the real estate industry but also mortgage lenders, investors, and the broader economy. While a correction in the housing market is a natural part of the economic cycle, a steep drop could lead to a cascade of negative effects.

Impact on the Real Estate Industry

A sharp decline in home prices would likely result in a slowdown in new home construction and a decrease in real estate transactions. This would affect builders, developers, and real estate agents, leading to job losses and reduced revenue. The reduced demand for new homes could also lead to an oversupply of inventory, further depressing prices.

Impact on Mortgage Lenders and Investors

Mortgage lenders could face increased losses due to defaults on loans as homeowners struggle to make payments in a declining market. Investors who hold mortgage-backed securities could also experience losses if the value of these securities falls due to higher default rates.

Impact on the Overall Economy

A significant home price drop could have a ripple effect on the overall economy. It could lead to a decrease in consumer spending, as homeowners feel less wealthy and are less likely to make large purchases. This could further dampen economic growth and lead to job losses in other sectors. Additionally, a decline in home prices could affect the value of collateral used for loans, leading to tighter credit conditions and making it more difficult for businesses to borrow money.

A study by the National Association of Realtors found that a 10% decline in home prices could lead to a 0.5% decrease in GDP growth.

Strategies for Navigating the Market: Wall Street Expects Second Biggest Home Price Drop Since Great Depression

The anticipated home price drop presents a unique set of challenges and opportunities for both homeowners and potential buyers. Understanding the potential impact of this downturn and adopting appropriate strategies can help mitigate risks and capitalize on emerging trends.

Strategies for Homeowners

Navigating a declining market requires proactive planning and informed decision-making. Here are some strategies for homeowners facing a potential price drop:

- Maintain Your Home: Regular maintenance can help preserve your home’s value and enhance its appeal to potential buyers. This includes addressing any necessary repairs, updating outdated fixtures, and keeping the property clean and well-maintained.

- Consider Refinancing: If interest rates have fallen since you took out your mortgage, refinancing could lower your monthly payments and potentially save you money over the long term. This can also help improve your cash flow and reduce the financial pressure of a potential price drop.

- Explore Selling Options: While the market may be challenging, selling now might be a good option if you need to relocate or are facing financial hardship. However, be prepared to adjust your expectations and potentially accept a lower selling price. Consider working with a real estate agent who has experience in a declining market.

- Hold Tight: If you are not in a hurry to sell, holding onto your property might be the best option. Waiting for the market to recover could potentially lead to a higher sale price in the future. This strategy requires patience and a strong financial position to weather the downturn.

Strategies for Buyers

A declining market presents a unique opportunity for buyers seeking a good deal. However, it’s crucial to proceed with caution and make informed decisions. Here are some strategies for navigating the buyer’s market:

- Secure Pre-Approval: Getting pre-approved for a mortgage before starting your search shows sellers you are a serious buyer and can help you move quickly on attractive properties. This also gives you a clear understanding of your budget and purchasing power.

- Negotiate Aggressively: With more properties on the market, buyers have more leverage to negotiate lower prices and favorable terms. Research comparable properties and be prepared to make a strong offer that reflects the current market conditions.

- Look for Motivated Sellers: Sellers facing financial difficulties or those needing to sell quickly might be more willing to accept lower offers. This could be a good opportunity to find a great deal on a desirable property.

- Be Patient: The market might take time to stabilize. Don’t rush into a purchase just because prices are falling. Take your time to find the right property that meets your needs and budget.

Impact and Strategies Table

The following table Artikels various scenarios, their potential impacts, recommended strategies, and expected outcomes for homeowners and buyers:

| Scenario | Potential Impact | Recommended Strategy | Expected Outcome |

|---|---|---|---|

| Homeowners facing a significant price drop | Reduced equity, potential for negative equity, difficulty selling at desired price | Consider refinancing to lower monthly payments, explore selling options, or hold tight and wait for market recovery | Improved cash flow, potential for higher sale price in the future, or minimizing financial losses |

| Buyers in a declining market | Lower prices, increased inventory, more negotiating power | Secure pre-approval, negotiate aggressively, look for motivated sellers, and be patient | Purchase of a desirable property at a lower price, better negotiating terms, potential for a higher return on investment in the future |

| Homeowners needing to sell quickly | Pressure to sell at a lower price, potential for financial losses | Work with a real estate agent specializing in declining markets, consider a short sale, or accept a lower selling price | Quick sale, potentially minimized financial losses, or access to needed funds |

| Buyers with a limited budget | Opportunity to purchase a property that was previously out of reach | Focus on properties in lower price ranges, negotiate aggressively, and be prepared to compromise on some features | Purchase of a property that aligns with budget, potentially higher return on investment in the future |

Historical Context and Market Cycles

Understanding the current housing market trends requires looking back at historical cycles and recognizing both the similarities and differences between past crashes and the present situation. Examining historical data helps us understand the potential duration and recovery timeline of the expected price drop.

Historical Market Cycles, Wall street expects second biggest home price drop since great depression

The housing market, like any other financial market, operates in cycles, marked by periods of growth, peak, decline, and recovery. Understanding these cycles helps us identify the current stage and anticipate potential future movements. Here are some notable historical examples of housing market cycles:

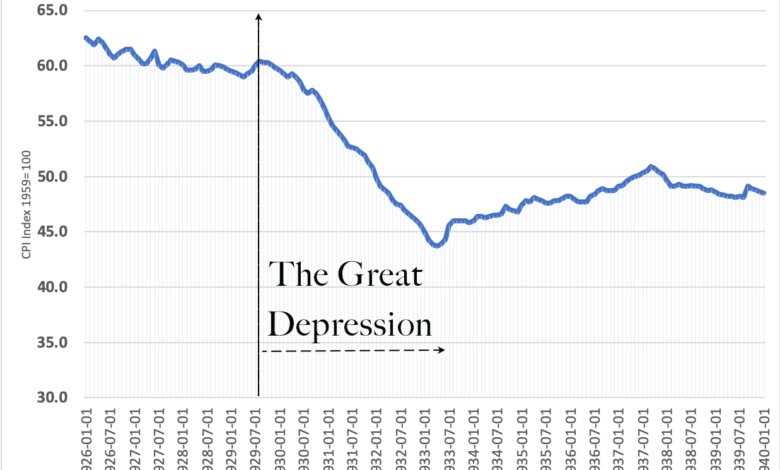

- The Great Depression (1929-1939): This period witnessed a dramatic decline in home prices, with a peak-to-trough drop of over 26%. The downturn was fueled by factors such as the stock market crash, bank failures, and widespread unemployment. Recovery was slow and uneven, taking several years for the market to stabilize.

- The Savings and Loan Crisis (1980s): This crisis was characterized by widespread failures of savings and loan associations, leading to a significant decline in housing construction and a drop in home prices. The crisis was triggered by factors such as deregulation of the savings and loan industry, high interest rates, and risky lending practices.

- The Housing Bubble and Bust (2000s): The early 2000s saw a rapid rise in home prices fueled by loose lending practices and speculation. This bubble eventually burst, leading to a severe decline in home prices, foreclosures, and the financial crisis of 2008. The recovery from this downturn was relatively slow and painful, with home prices taking several years to rebound.

Navigating this turbulent market requires careful planning and strategic thinking. Whether you’re a homeowner facing a potential price drop or a buyer looking to enter the market, understanding the factors driving this shift and considering available strategies is crucial. The current housing market landscape presents both challenges and opportunities, and a proactive approach can help you weather the storm and emerge with your financial goals intact.