Taxation in the US: From Inception to Today

The history of taxation in the United States from inception to modern day policy is a fascinating journey through the evolution of a nation. From the early colonial days to the complexities of the modern tax code, taxes have played a crucial role in shaping the American landscape.

This journey encompasses the challenges of financing colonial governments, the rise of a powerful federal system, and the social and economic transformations that have shaped the nation.

This blog post will delve into the historical development of taxation in the US, examining the key milestones, the impact of various tax policies, and the ongoing debates surrounding tax reform. We will explore how taxes have influenced the economy, social welfare programs, and the distribution of wealth throughout American history.

Early Taxation in Colonial America (1600s-1700s)

The early American colonies relied on a variety of taxes to finance their governments and infrastructure. These taxes, often levied by local assemblies, played a crucial role in shaping colonial society and laying the foundation for the future American tax system.

Forms of Taxation in the Colonies

The primary forms of taxation in the colonies included:

- Property Taxes:These were the most common form of taxation, levied on land, buildings, and other forms of real estate. These taxes were often assessed based on the value of the property and used to fund local government services like roads, schools, and law enforcement.

- Poll Taxes:These taxes were levied on individuals, regardless of their wealth or property ownership. They were often used to fund local services like the militia or to provide relief to the poor.

- Excise Taxes:These taxes were levied on the sale of specific goods, such as liquor, tobacco, or imported goods. These taxes were often used to generate revenue for the colonial governments.

- Duties and Tariffs:These taxes were levied on imported goods and were used to generate revenue and protect local industries.

Financing Colonial Governments and Infrastructure

Taxes were essential for funding colonial governments and infrastructure. They financed:

- Government Operations:Taxes funded the salaries of colonial officials, the cost of maintaining courts, and other administrative expenses.

- Public Works:Taxes were used to fund the construction and maintenance of roads, bridges, and other public works projects, which were essential for trade and transportation.

- Military Defense:Taxes were used to fund the colonial militia, which was responsible for defending the colonies from attacks by Native Americans, European rivals, and pirates.

- Education and Social Welfare:In some colonies, taxes were used to fund schools and provide relief to the poor.

Tax Systems of Different Colonies

The tax systems of the different colonies varied significantly. Some colonies, like Virginia, relied heavily on property taxes, while others, like Pennsylvania, relied more on excise taxes. The specific taxes levied and the methods of collection differed depending on the needs and resources of each colony.

Examples of Colonial Tax Laws and their Impact

Several examples illustrate the impact of colonial tax laws on the population.

- The Stamp Act (1765):This British law imposed a tax on printed materials, such as newspapers, legal documents, and playing cards. It was met with widespread resistance in the colonies, leading to boycotts and protests. The Stamp Act was eventually repealed, but it contributed to the growing tensions between the colonies and Great Britain.

- The Tea Act (1773):This British law granted the East India Company a monopoly on tea sales in the colonies. It was seen as a way to circumvent colonial taxes and generate revenue for the British government. The colonists responded with the Boston Tea Party, a protest that involved dumping tea into Boston Harbor.

Taxation Under the Articles of Confederation (1781-1789): The History Of Taxation In The United States From Inception To Modern Day Policy

The Articles of Confederation, adopted in 1781, established a weak central government with limited powers, including the ability to tax. This period witnessed significant challenges in funding the new nation and managing its finances.The Confederation government’s ability to levy taxes was severely restricted.

The Articles of Confederation granted Congress the power to request funds from the states, but it lacked the authority to directly tax individuals or businesses. This limitation stemmed from the colonists’ fear of a strong central government that could potentially abuse its power, as they had experienced under British rule.

Challenges in Raising Revenue

The Confederation government faced significant challenges in raising revenue due to its limited taxing authority.

- The states were reluctant to contribute their fair share of funds, often prioritizing their own interests over the national good.

- The lack of a uniform tax system across the states created disparities in revenue collection and further complicated the financial situation.

- The government’s inability to enforce tax collection led to widespread tax evasion, further exacerbating its financial woes.

Impact on the Economy

The absence of a strong central taxing authority had a detrimental impact on the economy.

- The government’s inability to finance its operations effectively hampered its ability to provide essential services, such as national defense and infrastructure development.

- The lack of a stable currency and a consistent system of taxation created uncertainty and instability in the marketplace.

- The government’s financial struggles led to a decline in public confidence and discouraged investment, further hindering economic growth.

Role of Taxation in the Emergence of the Constitutional Convention

The shortcomings of the Articles of Confederation, particularly the lack of a strong central taxing authority, played a crucial role in the emergence of the Constitutional Convention. The financial crisis faced by the Confederation government highlighted the need for a more robust and centralized system of governance.

The delegates to the Constitutional Convention recognized the importance of a strong national government with the power to tax, regulate commerce, and ensure the stability of the nation’s finances.

The US Constitution and the Power to Tax (1789-Present)

The US Constitution, adopted in 1787, established a new framework for governance, including the crucial power to tax. This power was carefully delineated between the federal and state governments, laying the foundation for the American tax system as we know it today.The Constitution’s framers recognized the importance of a strong central government with the ability to raise revenue for national defense, infrastructure, and other essential functions.

From the early days of the American colonies, taxation has played a crucial role in shaping our nation’s development. While the fight against “taxation without representation” sparked the Revolution, the need for revenue has continued to drive policy, evolving from tariffs and excise taxes to the complex modern system of income and property taxes.

It’s a reminder that even in the face of tragedies like the recent attack on LA deputies, new details on condition of la deputies attacked in patrol car huge reward offered for info on triggerman , the ongoing debate over how to fairly fund our government and services remains at the forefront of American discourse.

At the same time, they sought to protect the sovereignty of individual states and their ability to govern themselves.

The Distribution of Taxing Powers

The Constitution grants the federal government the power to levy taxes through Article I, Section 8, Clause 1, which states: “The Congress shall have Power To lay and collect Taxes, Duties, Imposts and Excises, to pay the Debts and provide for the common Defence and general Welfare of the United States.” This clause establishes the broad scope of federal taxing authority, allowing Congress to impose taxes on a wide range of activities and transactions.However, the Constitution also acknowledges the taxing powers of individual states.

The Tenth Amendment reserves to the states all powers not specifically delegated to the federal government, including the power to tax. This division of taxing powers creates a complex system where both the federal and state governments can impose taxes on the same individuals and businesses.

The Constitution provides some guidelines for this co-existence, ensuring that federal taxes are not levied on state governments or their instrumentalities, and vice versa.

Direct and Indirect Taxes

The Constitution distinguishes between “direct” and “indirect” taxes, a distinction that has played a significant role in shaping American tax law.

“Direct Taxes shall be apportioned among the several States which may be included within this Union, according to their respective Numbers.”

Direct taxes are levied directly on individuals or property, such as income taxes or property taxes. Indirect taxes, on the other hand, are levied on goods or services and are ultimately passed on to consumers, such as excise taxes on gasoline or sales taxes.The distinction between direct and indirect taxes has been subject to much debate and legal interpretation throughout American history.

Early Supreme Court rulings, such as the landmark case of Hylton v. United States(1796), defined direct taxes as those levied on land and capitation (head) taxes, while indirect taxes were considered those levied on goods and services.

Early Federal Tax Laws

The first federal tax laws passed under the Constitution were largely focused on raising revenue for the new nation’s burgeoning needs.

- The Tariff Act of 1789:This act established tariffs on imported goods, a key source of revenue for the early federal government. Tariffs, also known as customs duties, are indirect taxes, levied on goods imported into the country. They are designed to raise revenue for the government and protect domestic industries from foreign competition.

- The Excise Tax Act of 1791:This act levied excise taxes on distilled spirits, a significant source of revenue at the time. Excise taxes are indirect taxes levied on the production, sale, or consumption of specific goods.

- The Direct Tax Act of 1798:This act levied direct taxes on land and slaves, a controversial measure that was met with resistance in some states. The direct tax was repealed in 1802, but it highlights the early federal government’s reliance on direct taxation during periods of need.

The Evolution of Federal Taxation (1789-1900)

The early years of the United States government were marked by a struggle to establish a stable and effective system of taxation. The founding fathers, wary of the heavy-handed tax policies of the British monarchy, initially favored limited government intervention in the economy and relied heavily on tariffs and excise taxes to generate revenue.

However, the challenges of financing a growing nation, coupled with the exigencies of war and economic crises, gradually led to the expansion of the federal tax base and the development of new tax instruments.

The Role of Tariffs and Excise Taxes

The first federal tax laws enacted in the United States primarily relied on tariffs and excise taxes. Tariffs, taxes levied on imported goods, were a significant source of revenue for the early republic. They were seen as a way to protect domestic industries from foreign competition while also generating revenue for the government.

Excise taxes, levied on the production or sale of specific goods like alcohol and tobacco, were another important source of revenue.

The Tariff Act of 1789, the first major piece of federal legislation, established a system of tariffs on imported goods, reflecting the importance of tariffs in financing the fledgling government.

The Impact of the Civil War

The Civil War (1861-1865) marked a turning point in the history of federal taxation. The enormous costs of the war forced the federal government to significantly expand its tax base and introduce new forms of taxation. The war led to the enactment of the first federal income tax in 1861, which levied a tax on incomes exceeding $800.

This income tax was temporary and was repealed after the war. However, it laid the groundwork for the later development of a permanent federal income tax.

The passage of the Internal Revenue Act of 1862, which imposed taxes on a wide range of goods and services, including income, marked a dramatic shift in federal tax policy, reflecting the financial pressures of the Civil War.

The history of taxation in the United States is a fascinating one, from the early days of the Stamp Act to the modern era of complex income tax codes. It’s a story of evolving needs, shifting priorities, and the constant tension between individual liberty and the demands of a functioning government.

This tension is perhaps most acutely felt in the context of free speech, as highlighted by the recent clinton meme trial could chill free speech for all americans attorney says. This case raises questions about the boundaries of acceptable expression, especially in the digital age, and how they intersect with the need for a stable and well-funded government.

The Rise of the Income Tax

The late 19th century witnessed the rise of industrialization and urbanization in the United States, leading to a growing gap between the rich and the poor. This growing inequality, coupled with the increasing demand for public services like education and infrastructure, fueled the movement for a progressive income tax, a tax system where higher earners pay a greater percentage of their income in taxes.

The Supreme Court’s ruling in Pollock v. Farmers’ Loan & Trust Co. (1895), which declared the income tax unconstitutional, represented a setback for progressive tax reform, but it also galvanized the movement for a constitutional amendment to allow for a federal income tax.

The Legacy of Early Federal Taxation

The period from 1789 to 1900 witnessed a significant evolution in federal taxation, from the reliance on tariffs and excise taxes to the introduction of the income tax. This evolution was driven by a combination of factors, including the need to finance a growing nation, the demands of war, and the increasing calls for social and economic reform.

These early developments laid the foundation for the modern federal tax system, which continues to evolve to meet the changing needs of the nation.

The Progressive Era and the Rise of Income Tax (1900-1930)

The early 20th century witnessed a profound shift in American society, marked by rapid industrialization, urbanization, and growing economic inequality. This era, known as the Progressive Era, saw a surge in social and political activism aimed at addressing these challenges.

One of the most significant reforms of this period was the emergence of the progressive income tax. The progressive income tax, a system where higher earners pay a larger proportion of their income in taxes, emerged as a response to the increasing wealth disparities and the perceived unfairness of the existing tax system.

The prevailing system, largely based on tariffs and excise taxes, disproportionately burdened the working class and lower-income individuals.

The Rationale Behind the Progressive Tax Structure

The rationale behind the progressive tax structure was rooted in the principles of social justice and economic fairness. Proponents argued that those with greater means should contribute more to the common good. This principle was based on the belief that wealthier individuals had a greater ability to pay and that their contributions were essential for funding public services and programs that benefited all members of society.

The Impact of the 16th Amendment on Federal Taxation

The 16th Amendment, ratified in 1913, played a pivotal role in establishing the federal government’s power to levy an income tax. Prior to the 16th Amendment, the Supreme Court had ruled that a direct federal income tax was unconstitutional. The amendment effectively overturned this ruling, paving the way for the implementation of a progressive income tax system.

The Social and Economic Consequences of the Income Tax

The introduction of the income tax had significant social and economic consequences. On the one hand, it provided the federal government with a substantial new source of revenue, enabling it to fund social programs, infrastructure projects, and other public services.

This expanded role of the federal government in providing for the welfare of its citizens had a profound impact on American society.

The New Deal and World War II (1930-1945)

The Great Depression and World War II profoundly impacted the U.S. tax system, leading to significant changes in both the scope and purpose of federal taxation. The New Deal era saw the expansion of federal taxation to address the economic crisis, while World War II further amplified the role of taxes in financing government spending and supporting the war effort.

The Expansion of Federal Taxation During the New Deal Era

The New Deal, President Franklin D. Roosevelt’s program to address the Great Depression, introduced a series of social welfare programs and infrastructure projects. To finance these initiatives, the federal government significantly expanded its tax base and introduced new taxes. The New Deal introduced new taxes, such as the Social Security tax, which was a payroll tax levied on both employers and employees to fund the Social Security program.

This program provided financial assistance to the elderly, unemployed, and disabled. Additionally, the New Deal saw a significant increase in the federal income tax rates, especially for high-income earners. This shift towards progressive taxation, where higher earners paid a larger proportion of their income in taxes, was intended to redistribute wealth and provide more resources for social programs.

The Role of Taxes in Financing Social Welfare Programs and Infrastructure Projects

The New Deal’s social welfare programs, such as Social Security and unemployment insurance, aimed to provide a safety net for those in need. These programs were funded through payroll taxes, which were levied on both employers and employees. The federal government also used taxes to finance infrastructure projects, such as the Tennessee Valley Authority (TVA), which aimed to improve the region’s economy and infrastructure.

The TVA was funded through a combination of government bonds and revenue from electricity sales.

The Impact of World War II on Federal Taxation and Government Spending

World War II further increased the role of federal taxation in financing government spending. To support the war effort, the government raised taxes significantly, including income taxes, corporate taxes, and excise taxes. These tax increases were used to fund military expenditures, including the production of weapons, ammunition, and equipment.

The Introduction of New Tax Policies to Finance Wartime Expenditures

To finance the war effort, the government introduced new tax policies, such as payroll taxes, to fund wartime expenditures. The government introduced a new payroll tax, the Victory Tax, which was a temporary tax levied on wages and salaries to fund the war effort.

This tax was designed to be progressive, with higher earners paying a larger proportion of their income in taxes. The government also introduced a number of excise taxes, such as taxes on cigarettes, alcohol, and gasoline, to raise revenue for the war effort.

The Post-War Era and the Rise of Social Welfare Programs (1945-1980)

The period following World War II saw a significant shift in the United States, marked by a booming economy, a growing middle class, and a new era of social reform. This era witnessed the expansion of the federal government’s role in providing social welfare programs, fundamentally changing the relationship between the government and its citizens.

The Expansion of Social Welfare Programs

The post-war era witnessed the creation and expansion of numerous social welfare programs designed to address the needs of a growing population and to ensure a safety net for those facing economic hardship. These programs aimed to provide economic security, promote social mobility, and enhance the quality of life for all Americans.

- The Social Security Act of 1935 was expanded to cover more workers, including farmers and domestic workers, and to provide benefits for survivors and the disabled. This expansion ensured a basic level of income for retirees and those who were unable to work.

- The GI Bill, passed in 1944, provided educational and housing benefits to returning veterans, helping them to transition back into civilian life and contributing to the post-war economic boom.

- The creation of Medicare and Medicaid in 1965 marked a significant expansion of the social safety net, providing health insurance for the elderly and low-income Americans. These programs helped to ensure access to healthcare for those who might otherwise struggle to afford it.

- The Civil Rights Act of 1964 and the Voting Rights Act of 1965 addressed racial inequality and discrimination, advancing the cause of social justice and equality.

- The Elementary and Secondary Education Act of 1965 provided federal funding for education, aimed at improving the quality of education for all children, particularly those from disadvantaged backgrounds.

The Role of Taxation in Funding Social Welfare Programs

The expansion of social welfare programs in the post-war era was made possible by increased government spending, financed largely through taxation. The federal government implemented a progressive tax system, where higher earners paid a larger percentage of their income in taxes.

This system helped to ensure that the burden of funding social welfare programs was distributed more equitably across different income levels.

The Impact of the Cold War on Federal Taxation and Government Spending, The history of taxation in the united states from inception to modern day policy

The Cold War significantly influenced federal taxation and government spending. The need to compete with the Soviet Union in the arms race and to support allies around the world led to a substantial increase in military spending. This, in turn, contributed to higher tax rates and a larger federal budget.

The Cold War also fueled the growth of the national security state, with increased spending on intelligence, defense, and foreign aid.

The Evolution of the Tax Code During the Post-War Era

The tax code underwent significant changes during the post-war era, reflecting the evolving priorities of the government and the changing economic landscape.

- The introduction of the Internal Revenue Code of 1954 simplified and consolidated the tax code, making it easier for taxpayers to understand and comply with tax laws.

- The Tax Reform Act of 1969 aimed to reduce tax loopholes and simplify the tax code, leading to lower taxes for many individuals and businesses.

- The Tax Reform Act of 1986, under President Ronald Reagan, significantly reduced tax rates, simplified the tax code, and eliminated numerous tax loopholes. This act aimed to stimulate economic growth by reducing the burden of taxation on individuals and businesses.

The Reagan Revolution and Tax Cuts (1980-2000)

The Reagan administration’s economic policies, often referred to as “Reaganomics,” were characterized by significant tax cuts and deregulation, aiming to stimulate economic growth. This period saw a shift from the Keynesian economic approach that dominated the post-war era to a more supply-side approach.

Reagan’s Tax Cut Policies and Their Impact on the Economy

Reagan’s tax cuts, enacted in 1981 and 1986, reduced income tax rates for individuals and corporations. These cuts were based on the theory of supply-side economics, which argued that lower taxes would lead to increased investment, productivity, and economic growth.

Proponents of this theory believed that tax cuts would stimulate economic activity by increasing disposable income, encouraging businesses to invest, and ultimately leading to higher tax revenue for the government.The impact of Reagan’s tax cuts on the economy is a subject of ongoing debate.

Supporters point to the economic expansion of the 1980s, with the unemployment rate falling from 7.5% in 1980 to 5.3% in 1989, and the GDP growth rate averaging 3.9% during this period. They argue that the tax cuts helped to stimulate economic growth, leading to job creation and increased prosperity.Critics argue that the tax cuts led to increased income inequality and a growing national debt.

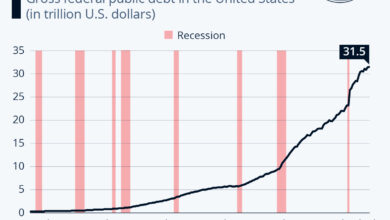

They point out that the benefits of the tax cuts disproportionately flowed to the wealthy, while the middle class and the poor saw little benefit. Additionally, the tax cuts led to significant budget deficits, which ultimately contributed to the national debt.

The Debate Over Tax Cuts and Their Effects on Income Inequality

The debate over tax cuts and their effects on income inequality is a complex one, with no easy answers. Supporters of tax cuts argue that they stimulate economic growth, which benefits everyone, including the poor. They argue that lower taxes create incentives for investment and job creation, leading to higher wages and more opportunities for all.Critics of tax cuts argue that they exacerbate income inequality by disproportionately benefiting the wealthy.

They point out that the wealthy are more likely to invest and save, while the poor are more likely to spend their income. This means that tax cuts tend to increase the wealth gap between the rich and the poor.

The Role of Supply-Side Economics in Shaping Tax Policy

Supply-side economics played a significant role in shaping tax policy during the Reagan era. This theory, which gained prominence in the 1970s, argues that economic growth is best achieved by stimulating production rather than demand. Supply-siders believe that government intervention in the economy, including high taxes and regulations, hinders economic growth.

They advocate for lower taxes, deregulation, and a free market approach to economic policy.Supply-side economics influenced Reagan’s tax cut policies, as well as other economic policies such as deregulation and cuts to social programs. While supply-side economics has been credited with helping to fuel the economic expansion of the 1980s, it has also been criticized for contributing to income inequality and the national debt.

Major Tax Laws Passed During the Reagan Era

Several major tax laws were passed during the Reagan era, including:

- Economic Recovery Tax Act of 1981 (ERTA): This act reduced individual income tax rates across the board, lowered the capital gains tax rate, and indexed the tax brackets for inflation. ERTA was a major component of Reagan’s supply-side economic policy.

- Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA): TEFRA was enacted to address the budget deficits that resulted from ERTA. It increased taxes on certain businesses and individuals, while also making some changes to social programs.

- Deficit Reduction Act of 1984 (DRA): DRA was another attempt to reduce the federal budget deficit. It included a combination of tax increases and spending cuts.

- Tax Reform Act of 1986 (TRA): TRA was a major overhaul of the federal tax code. It simplified the tax system by reducing the number of tax brackets and eliminating many deductions and loopholes. TRA also lowered the top marginal tax rate from 50% to 28%.

The history of taxation in the United States is a fascinating one, evolving from the early days of the nation to the complex system we see today. From the Stamp Act to the modern income tax, the way we fund government has changed dramatically.

This complex landscape is further impacted by current political trends, as seen in the recent article on the Arnnon Mishkin Trump vs Biden race which discusses the potential for shifting political power. Understanding these shifts is crucial for predicting the future of taxation in the United States, as it will undoubtedly influence the priorities and policies of the government.

These tax laws had a significant impact on the US economy and tax system. They helped to reduce the top marginal tax rate, stimulate investment, and simplify the tax code. However, they also contributed to the national debt and increased income inequality.

The 21st Century and Modern Tax Policy (2000-Present)

The 21st century has seen significant shifts in US tax policy, driven by factors such as globalization, technological advancements, and evolving economic priorities. These shifts have resulted in major tax laws being passed, debates over tax reform, and a constant evolution of the tax system to address contemporary challenges.

Major Tax Laws of the 21st Century

The early 2000s witnessed a series of tax cuts under President George W. Bush, aimed at stimulating economic growth. These tax cuts, enacted in 2001 and 2003, reduced income tax rates for all brackets, expanded the child tax credit, and lowered the estate tax.

The Bush tax cuts were controversial, with critics arguing that they disproportionately benefited the wealthy and contributed to the national debt.The Affordable Care Act (ACA), enacted in 2010, introduced a number of tax-related provisions, including a new individual mandate penalty for those without health insurance, tax credits for individuals purchasing health insurance through the marketplaces, and taxes on high-cost health insurance plans.

The ACA’s tax provisions were intended to fund the expansion of health insurance coverage and promote affordability.In 2017, the Tax Cuts and Jobs Act (TCJA) was enacted, representing the most significant tax reform legislation in decades. The TCJA reduced corporate tax rates, lowered individual income tax rates, expanded the standard deduction, and made changes to the estate tax.

The TCJA’s long-term impact on the economy and federal budget remains a subject of debate.

Impact of Globalization and Technological Advancements

Globalization has presented challenges for tax policy, as businesses increasingly operate across national borders. This has led to debates over the taxation of multinational corporations, transfer pricing, and the need for international tax coordination.Technological advancements have also had a profound impact on tax policy.

The rise of the internet and digital economy has created new challenges for taxing online businesses, as well as for collecting taxes from individuals working remotely. The use of artificial intelligence and data analytics is also transforming tax administration, with governments using these technologies to improve efficiency and combat tax evasion.

The Current Debate Over Tax Reform

The debate over tax reform in the US is ongoing, with different perspectives on the role of taxes in the economy, the distribution of the tax burden, and the appropriate level of government spending. One key issue is the distribution of the tax burden.

Some argue that the current tax system is too progressive, meaning that high-income earners pay a disproportionate share of taxes. Others argue that the system is not progressive enough, and that more needs to be done to address income inequality.Another key issue is the role of taxes in economic growth.

Some argue that lower taxes stimulate economic growth by increasing investment and consumer spending. Others argue that higher taxes are necessary to fund public goods and services that promote economic growth.

Key Features of Modern US Tax Policy

| Feature | Description |

|---|---|

| Progressive Income Tax System | Individuals with higher incomes pay a higher percentage of their income in taxes. |

| Payroll Taxes | Taxes levied on wages and salaries to fund Social Security and Medicare. |

| Corporate Income Tax | Tax levied on the profits of corporations. |

| Sales Taxes | Taxes levied on the sale of goods and services. |

| Property Taxes | Taxes levied on the value of real estate. |

Closing Summary

The history of taxation in the United States is a testament to the dynamic relationship between government, citizens, and the economy. From the early colonial days to the present, taxes have been a constant source of debate and change. As the nation continues to evolve, the debate over tax policy will undoubtedly remain a central issue.

Understanding the historical context of taxation provides valuable insights into the current landscape and the challenges we face in shaping a fair and equitable tax system for the future.