Rent to Own in the New Economy: A Shifting Landscape

Rent to own in the new economy is more than just a trend; it’s a reflection of changing financial realities and a growing desire for flexibility. The traditional path to homeownership, with its hefty down payments and stringent credit requirements, is becoming increasingly out of reach for many.

Rent-to-own offers an alternative, a way to build equity over time while enjoying the stability of a fixed monthly payment. But, as with any financial decision, there are pros and cons to consider, and the landscape of rent-to-own is constantly evolving.

This shift towards rent-to-own is driven by a confluence of factors, including rising housing costs, a changing workforce, and the growing popularity of subscription models. Rent-to-own offers a solution to these challenges, providing a path to ownership for those who might otherwise be locked out of the market.

However, it’s crucial to understand the financial implications and legal considerations before diving into a rent-to-own agreement.

Rent-to-Own in Different Sectors

The rent-to-own model has gained significant traction in recent years, offering consumers an alternative to traditional ownership models. This approach allows individuals to access goods and services while gradually paying for them over time, ultimately leading to ownership. This article will delve into the application of rent-to-own models in various sectors, analyzing their advantages and disadvantages, exploring successful programs, and discussing their potential impact on traditional ownership models.

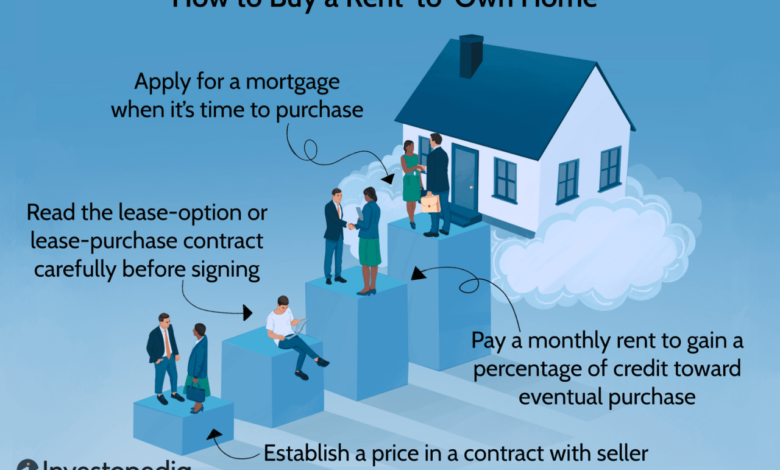

Housing

Rent-to-own programs in the housing sector offer a pathway to homeownership for individuals who may not qualify for traditional mortgages or prefer a more gradual approach to homebuying. These programs typically involve a lease agreement with an option to purchase the property at a predetermined price after a set period.

Advantages of Rent-to-Own in Housing

- Improved Access to Homeownership:Rent-to-own programs can open doors to homeownership for individuals who may not meet traditional mortgage requirements, such as those with limited credit history or lower incomes.

- Gradual Financial Commitment:By paying rent over time, individuals can gradually build equity in the property and prepare for eventual ownership, making the financial transition smoother.

- Time to Build Credit:Rent-to-own programs can provide an opportunity to build credit history, potentially making it easier to secure a mortgage in the future.

Disadvantages of Rent-to-Own in Housing

- Higher Overall Costs:Rent-to-own programs often come with higher overall costs compared to traditional mortgages, including potentially higher rent payments and a purchase option price that may exceed the market value.

- Limited Flexibility:Rent-to-own agreements often involve a fixed purchase price and a set timeframe, limiting flexibility if circumstances change, such as a job relocation or financial hardship.

- Risk of Losing Investment:If an individual is unable to complete the purchase option, they may lose all payments made towards the property, potentially resulting in a significant financial loss.

Examples of Successful Rent-to-Own Programs in Housing

- Home Partners of America:This company partners with landlords and homeowners to offer rent-to-own options, providing a platform for connecting potential buyers with properties.

- Option to Purchase Agreements:Some landlords offer option to purchase agreements as part of their lease terms, allowing tenants to exercise the option to buy the property after a specified period.

Impact of Rent-to-Own on Traditional Ownership Models in Housing

Rent-to-own programs can potentially impact traditional ownership models by providing an alternative path to homeownership for individuals who may not qualify for traditional mortgages. This could lead to increased competition for properties and potentially higher prices in certain markets.

Rent-to-own programs are becoming increasingly popular in the new economy, offering a path to homeownership for those who might not qualify for a traditional mortgage. This shift towards flexible ownership models is a sign of the times, much like the recent revelation of the truth about the Russia hoax, as reported in this article.

Just as the truth about the Russia hoax has finally come to light, rent-to-own options are shedding light on new ways to achieve the dream of homeownership.

However, rent-to-own programs also have the potential to increase housing affordability for certain segments of the population, making homeownership more accessible.

Automobiles, Rent to own in the new economy

Rent-to-own programs in the automotive industry offer a way to access vehicles without upfront costs, providing an alternative to traditional financing options. These programs typically involve a lease agreement with an option to purchase the vehicle at a predetermined price after a set period.

Advantages of Rent-to-Own in Automobiles

- Access to Vehicles with Limited Credit:Rent-to-own programs can make vehicles accessible to individuals with limited credit history who may not qualify for traditional financing.

- Lower Down Payment:Rent-to-own programs often require a lower down payment compared to traditional financing, making it easier to get into a vehicle.

- Flexibility:Rent-to-own agreements typically offer flexibility in terms of lease length and purchase options, allowing individuals to tailor the program to their specific needs.

Disadvantages of Rent-to-Own in Automobiles

- Higher Overall Costs:Rent-to-own programs often come with higher overall costs compared to traditional financing, including potentially higher monthly payments and a purchase option price that may exceed the market value.

- Limited Vehicle Choices:Rent-to-own programs may offer a limited selection of vehicles, typically focusing on older or used models.

- Risk of Losing Investment:If an individual is unable to complete the purchase option, they may lose all payments made towards the vehicle, potentially resulting in a significant financial loss.

Examples of Successful Rent-to-Own Programs in Automobiles

- ACME Rent-to-Own:This company offers a variety of rent-to-own programs for vehicles, including options for both new and used models.

- Rent-A-Center:While primarily known for furniture and electronics, Rent-A-Center also offers rent-to-own programs for vehicles in certain locations.

Impact of Rent-to-Own on Traditional Ownership Models in Automobiles

Rent-to-own programs can potentially impact traditional ownership models by providing an alternative path to vehicle ownership for individuals who may not qualify for traditional financing. This could lead to increased competition for used vehicles and potentially higher prices in certain segments of the market.

However, rent-to-own programs also have the potential to increase vehicle affordability for certain segments of the population, making vehicle ownership more accessible.

Electronics

Rent-to-own programs in the electronics sector offer a way to access the latest gadgets and appliances without upfront costs, providing an alternative to traditional purchase or financing options. These programs typically involve a lease agreement with an option to purchase the device at a predetermined price after a set period.

Advantages of Rent-to-Own in Electronics

- Access to Latest Technology:Rent-to-own programs allow individuals to access the latest electronics without having to pay the full upfront cost, enabling them to stay current with technological advancements.

- Flexibility:Rent-to-own agreements typically offer flexibility in terms of lease length and purchase options, allowing individuals to upgrade to newer models or return the device if their needs change.

- Lower Monthly Payments:Rent-to-own programs often involve lower monthly payments compared to traditional financing, making it more affordable to access high-priced electronics.

Disadvantages of Rent-to-Own in Electronics

- Higher Overall Costs:Rent-to-own programs often come with higher overall costs compared to traditional purchase or financing options, including potentially higher monthly payments and a purchase option price that may exceed the market value.

- Limited Device Selection:Rent-to-own programs may offer a limited selection of devices, typically focusing on popular models or those with a proven track record.

- Risk of Losing Investment:If an individual is unable to complete the purchase option, they may lose all payments made towards the device, potentially resulting in a significant financial loss.

Examples of Successful Rent-to-Own Programs in Electronics

- Rent-A-Center:This company offers a wide range of rent-to-own programs for electronics, including televisions, computers, and gaming consoles.

- Aaron’s:Similar to Rent-A-Center, Aaron’s offers rent-to-own programs for electronics, as well as furniture and appliances.

Impact of Rent-to-Own on Traditional Ownership Models in Electronics

Rent-to-own programs can potentially impact traditional ownership models by providing an alternative path to electronics ownership for individuals who may not have the financial means to purchase them outright. This could lead to increased competition for used electronics and potentially lower prices in certain segments of the market.

However, rent-to-own programs also have the potential to increase access to technology for certain segments of the population, bridging the digital divide and promoting technological inclusion.

Rent-to-own options are becoming increasingly popular in the new economy, offering flexibility and affordability for those seeking to own assets like homes or vehicles. But just as these models provide a path to ownership, the rapid shift to renewable energy sources raises concerns about grid reliability, a critical component of our modern infrastructure.

As highlighted in this recent article, rush to renewables a risky gamble for americas electric grid , ensuring a stable and reliable power supply is essential for supporting these new economic models and the broader society.

Furniture

Rent-to-own programs in the furniture sector offer a way to furnish homes without upfront costs, providing an alternative to traditional purchase or financing options. These programs typically involve a lease agreement with an option to purchase the furniture at a predetermined price after a set period.

Advantages of Rent-to-Own in Furniture

- Furnishing Homes Without Upfront Costs:Rent-to-own programs allow individuals to furnish their homes without having to pay the full upfront cost, making it more affordable to create a comfortable living space.

- Flexibility:Rent-to-own agreements typically offer flexibility in terms of lease length and purchase options, allowing individuals to upgrade to newer furniture or return pieces if their needs change.

- Lower Monthly Payments:Rent-to-own programs often involve lower monthly payments compared to traditional financing, making it more affordable to furnish a home.

Disadvantages of Rent-to-Own in Furniture

- Higher Overall Costs:Rent-to-own programs often come with higher overall costs compared to traditional purchase or financing options, including potentially higher monthly payments and a purchase option price that may exceed the market value.

- Limited Furniture Selection:Rent-to-own programs may offer a limited selection of furniture, typically focusing on popular styles or those with a proven track record.

- Risk of Losing Investment:If an individual is unable to complete the purchase option, they may lose all payments made towards the furniture, potentially resulting in a significant financial loss.

Examples of Successful Rent-to-Own Programs in Furniture

- Rent-A-Center:This company offers a wide range of rent-to-own programs for furniture, including sofas, beds, and dining sets.

- Aaron’s:Similar to Rent-A-Center, Aaron’s offers rent-to-own programs for furniture, as well as electronics and appliances.

Impact of Rent-to-Own on Traditional Ownership Models in Furniture

Rent-to-own programs can potentially impact traditional ownership models by providing an alternative path to furniture ownership for individuals who may not have the financial means to purchase them outright. This could lead to increased competition for used furniture and potentially lower prices in certain segments of the market.

However, rent-to-own programs also have the potential to increase access to affordable furniture for certain segments of the population, improving living standards and creating more comfortable living spaces.

Financial Implications of Rent-to-Own: Rent To Own In The New Economy

Rent-to-own arrangements offer a unique path to homeownership, but it’s crucial to understand the financial implications for both renters and landlords. This arrangement involves paying rent with the option to purchase the property at a predetermined price in the future.

The concept of rent-to-own is becoming increasingly popular in the new economy, especially with the rising cost of living. It offers a path to homeownership for those who might not be able to afford a traditional mortgage. However, it’s important to remember that even in a seemingly safe environment like Times Square, incidents like the machete attack near Times Square on New Year’s Eve that left two NYPD officers injured can happen, reminding us that security is a shared responsibility.

It’s crucial to be aware of your surroundings and consider all aspects of your financial situation before making a significant commitment like rent-to-own.

While it can be appealing for renters seeking homeownership, it’s essential to carefully analyze the financial aspects to make an informed decision.

Cost Comparison with Traditional Financing

Rent-to-own arrangements often come with higher overall costs compared to traditional mortgage financing. The initial rent payments may include a portion allocated toward the future purchase price, known as the “option fee.” Additionally, the purchase price may be higher than the market value, reflecting the landlord’s profit margin.

- Rent-to-own:Rent payments include an option fee, and the purchase price may be higher than market value.

- Traditional financing:Requires a down payment, closing costs, and ongoing mortgage payments.

For example, let’s consider a property with a market value of $200,000. A rent-to-own agreement might require a monthly rent of $1,500, including a $500 option fee. After five years, the purchase price could be $220,000, representing a 10% markup.

In contrast, a traditional mortgage with a 20% down payment ($40,000) and a 30-year fixed-rate mortgage at 4% would result in a monthly payment of approximately $955. While the rent-to-own option offers a lower upfront cost, the overall cost can be significantly higher due to the option fee and potential markup on the purchase price.

Potential for Financial Instability or Empowerment

Rent-to-own arrangements can present both financial instability and empowerment opportunities. The potential for instability stems from the possibility of defaulting on rent payments, leading to the loss of the option to purchase. This could result in financial losses for the renter, including the option fee and any accumulated rent payments allocated towards the purchase price.

However, rent-to-own can also empower renters by providing a pathway to homeownership, especially for those with limited access to traditional financing. The option to purchase can offer a sense of security and stability, allowing renters to build equity over time.

Strategies for Mitigating Financial Risks

To mitigate financial risks associated with rent-to-own, renters should carefully consider the following strategies:

- Thorough research:Analyze the market value of the property, compare the purchase price with similar properties, and understand the terms of the rent-to-own agreement, including the option fee, purchase price, and any penalties for default.

- Financial planning:Ensure you have a solid financial plan that includes budgeting for rent payments, saving for the down payment, and managing potential unexpected expenses.

- Negotiation:Consider negotiating the terms of the agreement, such as the option fee, purchase price, and any penalties for default.

- Legal counsel:Consult with a lawyer to review the rent-to-own agreement and understand your legal rights and obligations.

Legal and Regulatory Considerations

Rent-to-own agreements, while offering a unique pathway to homeownership, are subject to a complex web of legal and regulatory frameworks. These frameworks aim to protect both consumers and businesses involved in these transactions, ensuring fairness and transparency.

Consumer Protection Issues

Rent-to-own contracts often involve complex financial structures and terms that can be difficult for consumers to understand. This complexity raises concerns about potential consumer protection issues.

- High Fees and Interest Rates:Rent-to-own agreements frequently involve substantial upfront fees, monthly payments that often include a portion of the purchase price, and high interest rates. These factors can lead to a situation where consumers end up paying significantly more for the property than its market value.

- Lack of Transparency:Rent-to-own agreements can be written in complex legal language, making it difficult for consumers to understand the terms and conditions. This lack of transparency can lead to unexpected costs and obligations.

- Limited Consumer Rights:In some cases, consumers may have limited rights to terminate the agreement or receive a refund if they decide not to purchase the property. This can leave consumers vulnerable to financial losses.

Government Policies

Governments play a crucial role in shaping the rent-to-own landscape by enacting regulations and policies to address consumer protection concerns.

- Disclosure Requirements:Many jurisdictions require landlords or sellers to provide detailed disclosures to potential renters outlining the terms and conditions of the agreement, including purchase options, fees, and interest rates. This helps ensure transparency and empowers consumers to make informed decisions.

- Cooling-Off Periods:Some regulations provide consumers with a cooling-off period during which they can terminate the agreement without penalty. This gives consumers time to reconsider their decision and avoid entering into contracts they may later regret.

- Rent-to-Own Regulations:Specific rent-to-own regulations may address issues such as maximum fees, interest rate caps, and requirements for escrow accounts to protect consumer deposits. These regulations aim to prevent predatory practices and ensure fair treatment of consumers.

Best Practices for Fair and Transparent Agreements

To ensure fair and transparent rent-to-own agreements, both landlords and consumers should follow best practices.

- Clear and Concise Agreements:Contracts should be written in plain language, avoiding jargon and technical terms that consumers may not understand. All terms and conditions, including purchase options, fees, and interest rates, should be clearly stated.

- Detailed Disclosures:Landlords or sellers should provide comprehensive disclosures outlining all relevant information about the property, including its condition, any known defects, and potential risks. This helps consumers make informed decisions.

- Escrow Accounts:Using escrow accounts to hold consumer deposits can protect consumers from potential misuse of funds. This ensures that deposits are held securely and used only for the intended purpose.

- Independent Legal Advice:Consumers should seek independent legal advice before entering into a rent-to-own agreement. This ensures that they understand their rights and obligations and can negotiate favorable terms.

Conclusive Thoughts

The future of rent-to-own is undoubtedly intertwined with technological advancements and evolving consumer preferences. As technology continues to disrupt traditional industries, we can expect to see innovative rent-to-own models emerge, catering to a wider range of needs and desires.

Whether it’s buying a home, a car, or even a piece of furniture, rent-to-own offers a flexible and accessible path to ownership, allowing individuals to achieve their financial goals while navigating the complexities of the new economy.