Ford Could Lock Out Owners for Missed Payments

Ford could lock out vehicle owners for missing loan payments under new patent – Ford Could Lock Out Owners for Missed Payments under new patent, a chilling prospect that has raised eyebrows across the automotive industry and sparked heated debates about consumer rights and ethical boundaries. This patent, which grants Ford the ability to remotely disable vehicles for unpaid loans, represents a significant shift in the power dynamics between car manufacturers and their customers.

The technology behind this feature, while not yet fully disclosed, likely involves sophisticated software and communication systems that allow Ford to access and control vehicle functions remotely. This raises serious concerns about privacy, security, and the potential for abuse.

The implications of this patent extend beyond the realm of finance. It raises questions about the potential for other car manufacturers to adopt similar technologies, creating a future where vehicles are not simply transportation but also tools for enforcing financial obligations.

Imagine a world where your car becomes inoperable due to a missed utility bill or a delayed credit card payment. This scenario, while seemingly far-fetched, is a stark reminder of the rapidly evolving landscape of automotive technology and its potential impact on our lives.

Ford’s New Patent and Vehicle Control

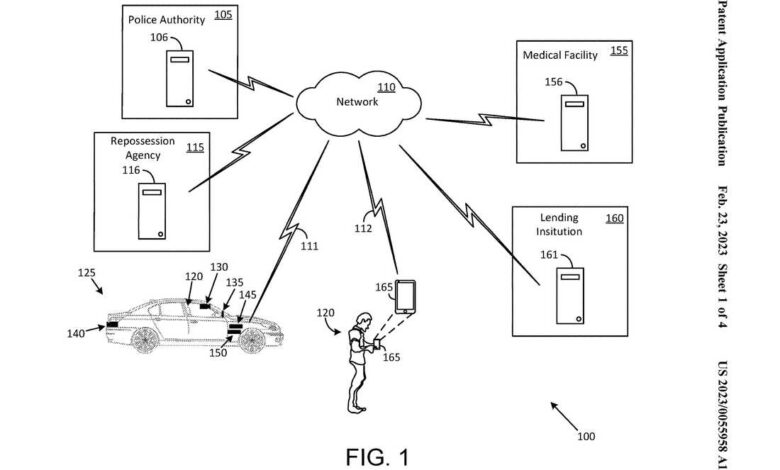

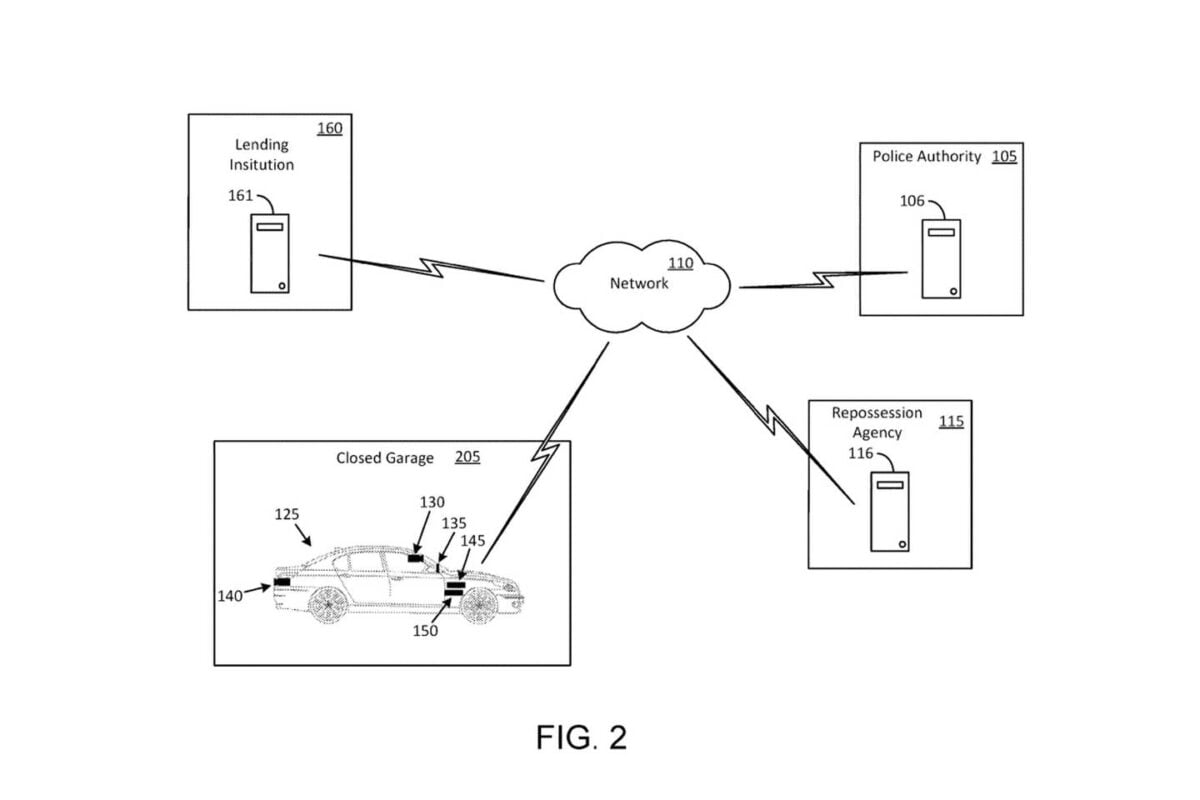

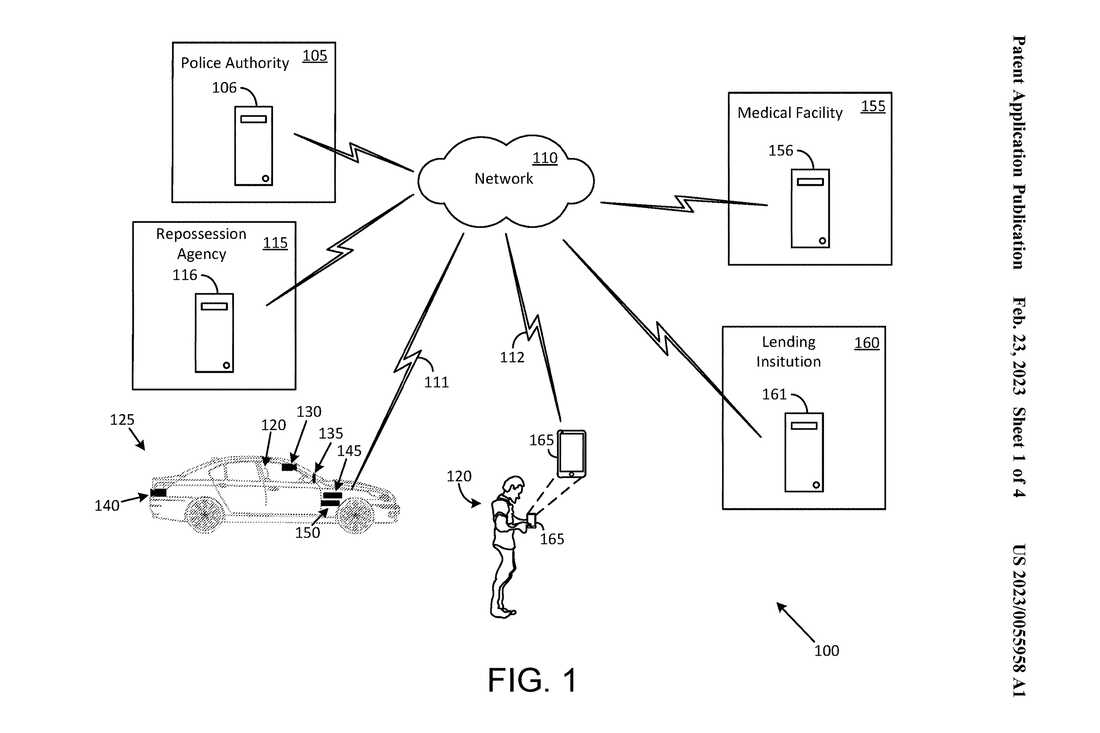

Ford has recently filed a patent for a system that would allow the automaker to remotely disable a vehicle if the owner misses loan payments. This patent, which is still under review, has raised concerns among car owners and consumer advocates about the potential for misuse and the implications for vehicle ownership.

Technology Behind the Patent

The patent details a system that uses telematics technology to monitor a vehicle’s location and status. This data is then used to determine if the owner is making their loan payments. If a payment is missed, the system can remotely disable the vehicle, preventing it from being driven.

Ford’s new patent for remotely disabling vehicles over missed loan payments is a stark reminder of the evolving power dynamics between corporations and consumers. While we grapple with the implications of such technology, it’s hard not to be reminded of the absurdity of Trump’s reaction to his Nobel Peace Prize nomination as “a great thing for our country.” Ford’s move raises serious questions about privacy and control, highlighting the need for careful consideration of how we navigate this increasingly digital world.

Potential Implications for Vehicle Owners

This patent raises a number of concerns for vehicle owners.

- The potential for misuse of the technology. If the system is not properly secured, it could be vulnerable to hacking, which could allow someone to disable a vehicle without authorization.

- The potential for the system to be used to harass or punish owners. For example, a lender could disable a vehicle even if the owner is only a few days late on a payment.

- The potential for the system to be used to control the vehicle’s use in ways that are not related to loan payments. For example, a lender could disable the vehicle if the owner drives it outside of a certain area.

Ford’s new patent allowing them to remotely disable vehicles for missed loan payments is a chilling reminder of the growing power corporations have over our lives. It’s a stark contrast to the ongoing struggle for democratic rights in Hong Kong, where police have arrested dozens of protesters as the government delays an elections report.

While Ford’s patent raises concerns about financial control, the situation in Hong Kong highlights the fight for basic freedoms. It’s a sobering reminder that we must remain vigilant against both corporate and political overreach.

Legal and Ethical Considerations

Ford’s patent for remotely disabling vehicles for missed loan payments raises significant legal and ethical concerns. This technology has the potential to impact consumer rights, privacy, and even public safety.

Consumer Rights and Privacy

The potential legal ramifications of Ford’s patent are significant. The ability to remotely disable a vehicle for non-payment raises concerns about consumer rights and privacy. The right to use a vehicle is a fundamental aspect of mobility and independence.

Remotely disabling a vehicle could leave individuals stranded, unable to get to work, school, or medical appointments. This could have severe consequences for their livelihood and well-being. Furthermore, the technology could be used to track vehicle location and usage patterns, raising concerns about privacy.

The potential for misuse of this data is a major concern, as it could be used for surveillance or other unauthorized purposes.

Ethical Implications of Remote Vehicle Disabling

The ethical implications of remotely disabling vehicles for financial reasons are equally troubling. This technology could be seen as a form of digital punishment, disproportionately affecting vulnerable populations who may be more likely to experience financial hardship. For example, individuals who have lost their jobs or are facing unexpected medical expenses may be unable to make their loan payments, leading to the disabling of their vehicles.

This could create a vicious cycle of financial hardship and limited mobility.Additionally, the technology could create a chilling effect on consumer behavior, discouraging individuals from seeking financial assistance or engaging in negotiations with lenders.

Comparison to Existing Practices, Ford could lock out vehicle owners for missing loan payments under new patent

The practice of remotely disabling vehicles for missed loan payments is not entirely unprecedented. Some companies have already implemented similar practices for other devices, such as smartphones and internet services. However, the implications of disabling a vehicle are far more significant, as it is a primary means of transportation for many individuals.

“The ability to remotely disable a vehicle for missed loan payments is a drastic measure that could have significant consequences for individuals and society as a whole.”

The potential for abuse and the lack of clear ethical guidelines raise serious concerns about the implementation of this technology. It is crucial for policymakers and industry leaders to carefully consider the potential consequences and develop appropriate regulations to protect consumer rights and ensure ethical use of this technology.

Ford’s new patent allowing them to remotely disable vehicles for missed loan payments raises serious questions about consumer rights and privacy. It’s a disturbing trend that echoes the recent revelations from a whistleblower who told Congress that the FBI leadership is “rotted at its core,” raising concerns about the potential for abuse of power.

We need to be vigilant about protecting our freedoms and holding corporations accountable for their actions, especially when it comes to controlling our personal property.

Consumer Impact and Reactions

The potential for Ford to remotely disable vehicles due to missed loan payments raises significant concerns about consumer impact and reactions. This technology could lead to a range of negative consequences, including heightened distrust between car manufacturers and customers, and the exacerbation of existing economic inequalities.

Potential Negative Reactions

The potential for a car manufacturer to remotely disable a vehicle due to missed loan payments could lead to a range of negative reactions from consumers.

- Fear and Anxiety:Many consumers might feel anxious and fearful about the prospect of losing access to their vehicle due to a missed payment, even if it is temporary. This fear could be heightened for individuals who rely on their vehicles for essential needs, such as work or transportation for medical appointments.

- Loss of Control:The ability of a manufacturer to remotely disable a vehicle could be perceived as a loss of control over one’s property. Consumers might feel frustrated and resentful at the idea that they are not fully in control of their vehicles.

- Privacy Concerns:Some consumers might worry about the privacy implications of this technology. The ability to remotely monitor and disable vehicles could raise concerns about data collection and potential misuse.

- Safety Concerns:In some cases, the remote disabling of a vehicle could create safety hazards. For example, if a vehicle is disabled while driving on a highway, it could lead to an accident.

Increased Distrust Between Car Manufacturers and Customers

The potential for Ford to remotely disable vehicles could lead to increased distrust between car manufacturers and customers. Consumers might view this technology as a power grab by manufacturers, who are using technology to exert more control over their customers.

This could lead to a decline in customer loyalty and a decrease in trust in the automotive industry as a whole.

Exacerbation of Economic Inequalities

The ability of car manufacturers to remotely disable vehicles due to missed loan payments could exacerbate existing economic inequalities. Individuals struggling financially might be more likely to miss loan payments, and they could be disproportionately affected by this technology. This could lead to a cycle of debt and hardship, as individuals are unable to access their vehicles and, as a result, lose their jobs or are unable to meet other essential needs.

Potential Alternatives and Solutions

Ford’s proposed patent for remotely disabling vehicles due to loan defaults raises serious concerns about consumer rights and potential consequences. While the company argues it aims to prevent vehicle theft, this method raises ethical and practical issues. Exploring alternative solutions is crucial to address loan defaults without resorting to vehicle immobilization.

Alternative Methods for Addressing Loan Defaults

Alternative methods for addressing loan defaults can be explored to protect both the interests of lenders and borrowers. These methods focus on financial and legal means to recover outstanding payments, minimizing the impact on vehicle functionality and consumer well-being.

- Financial Counseling and Debt Management Programs:Lenders can offer financial counseling services to borrowers facing financial difficulties. These programs can help borrowers develop personalized budgets, explore debt consolidation options, and navigate repayment plans. This approach promotes responsible borrowing and helps borrowers regain financial stability.

- Negotiated Repayment Plans:Lenders can work with borrowers to create customized repayment plans that consider their financial situation. These plans can include extended payment terms, reduced monthly payments, or temporary payment deferrals. This flexibility allows borrowers to manage their debts effectively without facing vehicle immobilization.

- Legal Recourse:Lenders can pursue legal avenues to recover unpaid loans, such as filing a lawsuit or seeking a court order for repossession. While this approach is a last resort, it provides a structured legal framework for debt recovery.

Solutions Balancing Lender and Borrower Interests

Finding solutions that balance the interests of both car manufacturers and consumers is essential to address loan defaults fairly. This requires exploring approaches that prioritize financial responsibility while safeguarding consumer rights and vehicle functionality.

- Enhanced Consumer Education and Transparency:Clear and comprehensive disclosure of loan terms, including the potential consequences of default, is crucial. Educating consumers about responsible borrowing practices and available resources can prevent defaults and empower borrowers to make informed decisions.

- Third-Party Mediation and Dispute Resolution:Establishing a neutral third-party entity to mediate disputes between lenders and borrowers can promote fair resolution. This platform can help facilitate communication, explore alternative solutions, and ensure transparency in the debt recovery process.

- Legislative Measures and Regulatory Oversight:Legislation and regulatory frameworks can establish clear guidelines for loan default management, ensuring that consumer rights are protected and lenders have fair access to debt recovery mechanisms. This can include limitations on vehicle immobilization, requirements for due process, and provisions for consumer protection.

Comparison of Approaches to Loan Default Management

The table below compares and contrasts different approaches to loan default management, highlighting their advantages and disadvantages.

| Approach | Advantages | Disadvantages |

|---|---|---|

| Vehicle Immobilization | Effective in preventing vehicle theft, potential for immediate debt recovery | Ethical concerns, negative impact on consumer well-being, potential for misuse, legal challenges |

| Financial Counseling and Debt Management Programs | Promotes responsible borrowing, helps borrowers regain financial stability, reduces risk of default | May not be effective for all borrowers, requires significant resources and commitment from lenders |

| Negotiated Repayment Plans | Provides flexibility for borrowers, minimizes financial hardship, promotes positive customer relationships | May not be feasible for all borrowers, potential for abuse, requires careful monitoring |

| Legal Recourse | Provides a structured legal framework for debt recovery, ensures fairness and transparency | Can be expensive and time-consuming, may not be effective for all borrowers, can damage borrower credit |

Concluding Remarks: Ford Could Lock Out Vehicle Owners For Missing Loan Payments Under New Patent

The Ford patent is a wake-up call, urging us to consider the ethical implications of technology that blurs the lines between personal property and financial instruments. While it’s crucial for lenders to protect their interests, doing so at the expense of consumer autonomy and privacy is a dangerous precedent.

This situation highlights the urgent need for open dialogue and transparent regulations to ensure that technological advancements in the automotive industry serve the best interests of both consumers and businesses. As connected vehicles become increasingly prevalent, the responsibility falls upon us to ensure that technology remains a tool for progress, not a weapon for control.