Hardship Withdrawals From 401k Plans Rise: A Warning Sign of Financial Distress

Hardship withdrawals from 401k plans rise in warning sign of financial distress sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with personal blog style and brimming with originality from the outset.

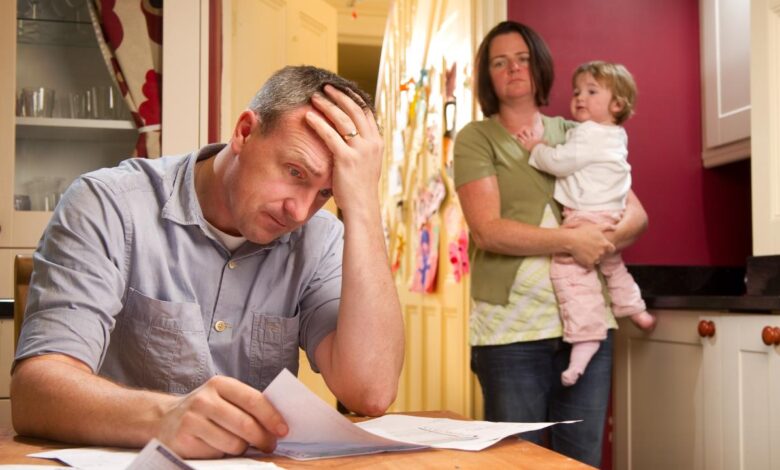

It’s a stark reality that many Americans are facing: financial emergencies are forcing them to dip into their retirement savings. The rise of hardship withdrawals from 401(k) plans is a troubling trend, reflecting a growing financial vulnerability among a significant portion of the population.

This trend is fueled by a confluence of economic factors, including soaring inflation, unexpected medical expenses, and job losses, all of which are pushing individuals to the brink of financial hardship.

The implications of these withdrawals extend far beyond the immediate need. Depleting retirement savings can have long-term consequences, potentially leading to reduced retirement income and delaying retirement plans. The impact of hardship withdrawals can vary significantly across demographic groups, with those facing financial instability, lower income levels, and those who are younger, experiencing greater vulnerability.

The consequences of these withdrawals can be severe, potentially jeopardizing individuals’ long-term financial security and leaving them facing a bleak future.

The Rise of Hardship Withdrawals: Hardship Withdrawals From 401k Plans Rise In Warning Sign Of Financial Distress

Hardship withdrawals from 401(k) plans have become increasingly common, signaling a growing trend of financial distress among Americans. These withdrawals, designed for emergencies, are now being utilized more frequently as individuals struggle to cope with economic pressures. This article delves into the reasons behind this surge in hardship withdrawals, examining the factors driving this trend and its implications for individual financial security.

Definition and Purpose of Hardship Withdrawals

Hardship withdrawals are special exceptions to the general rule that withdrawals from 401(k) plans are not allowed before age 59 1/2 without penalty. They are designed to provide financial relief in situations of immediate and severe financial need. These situations typically include:

- Medical expenses exceeding 10% of an individual’s adjusted gross income

- Loss of home due to fire, flood, or other natural disaster

- Payment of certain educational expenses for the individual, their spouse, or their dependents

- Prevention of eviction or foreclosure

- Expenses related to the purchase of a primary residence

It is important to note that hardship withdrawals are subject to strict eligibility requirements and are only permitted in cases of true financial hardship. The process typically involves providing documentation to support the claim, and the funds are usually subject to income tax and a 10% early withdrawal penalty.

Statistics on the Increase in Hardship Withdrawals

Data from the Employee Benefit Research Institute (EBRI) reveals a significant increase in hardship withdrawals in recent years. In 2022, 1.8% of 401(k) plan participants took hardship withdrawals, marking a substantial rise from 1.2% in 2019. This increase reflects the growing financial pressures faced by Americans, particularly in the wake of the COVID-19 pandemic.

Economic Factors Contributing to the Rise of Hardship Withdrawals

Several economic factors have contributed to the increase in hardship withdrawals, including:

- Inflation:The rising cost of living, fueled by persistent inflation, has put a strain on household budgets, forcing many individuals to dip into their retirement savings to cover basic expenses.

- Job Losses:Economic downturns and layoffs can lead to sudden income loss, pushing individuals to rely on their 401(k) plans for survival.

- Unexpected Medical Expenses:Unforeseen medical emergencies can result in significant out-of-pocket costs, forcing individuals to withdraw from their retirement savings to cover these expenses.

The combination of these economic factors has created a perfect storm for increased hardship withdrawals. Individuals are finding it increasingly difficult to manage their finances and are turning to their retirement savings as a last resort.

Financial Distress and Its Impact

Hardship withdrawals, while seemingly offering a lifeline during tough times, can have significant long-term consequences for individuals and their financial security. These withdrawals, often taken to cover immediate expenses, can erode retirement savings, potentially leading to a less comfortable retirement or even delaying retirement altogether.

Impact on Retirement Security

Depleting retirement savings through hardship withdrawals can have a substantial impact on an individual’s long-term financial security. Here’s how:

- Reduced Retirement Income:The primary purpose of retirement savings is to provide income during retirement. Withdrawing funds from a 401(k) reduces the amount available for investment, potentially leading to lower returns and a smaller nest egg in the future. This can translate into a reduced monthly income during retirement, forcing individuals to rely on other sources, such as Social Security or part-time work, to make ends meet.

- Delayed Retirement:Individuals who deplete their retirement savings through hardship withdrawals may find themselves unable to retire when they initially planned. The reduced nest egg may require them to work longer to accumulate enough funds for retirement, delaying their ability to enjoy their golden years.

- Financial Vulnerability:Hardship withdrawals can leave individuals financially vulnerable in the long run. They may be forced to rely on credit cards or other forms of debt to cover expenses, further increasing their financial burden and potentially impacting their credit score.

Impact on Different Demographic Groups

The impact of hardship withdrawals can vary depending on factors such as age, income level, and employment status.

- Age:Younger individuals who take hardship withdrawals may have more time to recover their savings, but the impact on their retirement income could still be significant. Older individuals who take hardship withdrawals face a more immediate challenge, as they have less time to rebuild their retirement savings.

The spike in hardship withdrawals from 401k plans is a stark reminder of the financial struggles many Americans are facing. It’s a situation that calls for thoughtful solutions, and while it might seem like a far cry from the world of billionaires, elon musk has an advice for jeff bezos check what , perhaps there are lessons to be learned from those at the top.

After all, even amidst unprecedented wealth, there’s a need to acknowledge the economic challenges faced by everyday people and strive for a more equitable system. This should be a wake-up call for us all to prioritize financial stability and build a more resilient future, especially in the face of such hardship withdrawals.

- Income Level:Individuals with lower incomes may be more likely to rely on hardship withdrawals, as they may have fewer resources to handle unexpected expenses. This can exacerbate their financial struggles and make it more difficult to achieve their retirement goals.

- Employment Status:Individuals who are unemployed or facing job insecurity may be more likely to turn to hardship withdrawals to cover essential expenses. This can leave them with less financial security during a period of already heightened vulnerability.

Alternatives to Hardship Withdrawals

Hardship withdrawals from your 401(k) can be a tempting solution when you’re facing a financial emergency, but they come with a hefty price tag. You’ll face taxes and penalties on the withdrawal, and you’ll be depleting your retirement savings, which could have serious consequences for your future financial security.

Luckily, there are alternative solutions you can explore before resorting to a hardship withdrawal. Before tapping into your retirement funds, consider these alternatives that can provide immediate relief without jeopardizing your long-term financial goals.

Emergency Savings

It’s crucial to have an emergency fund that can cover unexpected expenses. This fund should ideally cover 3-6 months of living expenses. If you don’t have an emergency fund, start building one as soon as possible by setting aside a small amount of money each month.

The rise in hardship withdrawals from 401k plans is a stark reminder of the economic pressures many Americans are facing. This trend, coupled with the recent downturn in the tech industry, amid global chaos the tech industry takes a rare tumble , is painting a grim picture of financial distress across the nation.

As the tech sector grapples with layoffs and uncertainty, the reliance on retirement savings for immediate needs highlights the growing vulnerability of many households.

Even a small amount can add up over time.

Financial Assistance Programs

Many government and non-profit organizations offer financial assistance programs to individuals facing hardship. These programs can provide grants, loans, or other forms of support to help with expenses such as rent, utilities, food, and medical bills.

- Government programs:The federal government offers a variety of programs to help individuals in need, such as SNAP (food stamps), TANF (Temporary Assistance for Needy Families), and LIHEAP (Low Income Home Energy Assistance Program).

- Non-profit organizations:Many non-profit organizations provide financial assistance to individuals in need. These organizations may offer grants, loans, or other forms of support. Some examples include the Salvation Army, United Way, and Catholic Charities.

Negotiating with Creditors

If you’re struggling to make payments on your bills, you can often negotiate with your creditors to make a payment plan or lower your interest rate. This can help you manage your debt and avoid late fees and penalties.

- Contact your creditors:Explain your situation and ask for a payment plan or a lower interest rate. Be polite and professional.

- Credit counseling agencies:These agencies can help you negotiate with creditors and create a budget to manage your debt. They can also provide advice on debt consolidation and other strategies for getting out of debt.

Loans

If you need a short-term loan, you can consider a personal loan, a home equity loan, or a 401(k) loan. These loans can provide you with the funds you need without depleting your retirement savings. However, it’s important to be aware of the interest rates and repayment terms before taking out a loan.

- Personal loans:These loans are typically unsecured, meaning they don’t require collateral. Interest rates vary depending on your credit score.

- Home equity loans:These loans are secured by your home equity. They typically have lower interest rates than personal loans, but you risk losing your home if you default on the loan.

- 401(k) loans:These loans allow you to borrow money from your 401(k) account. You’ll need to repay the loan with interest, but the interest you pay goes back into your 401(k) account.

Credit Cards

Credit cards can be a useful tool for managing unexpected expenses, but they should be used responsibly. If you have a good credit score, you may be able to get a low-interest credit card. However, it’s important to make your payments on time to avoid high interest charges and late fees.

Comparison of Financial Assistance Options, Hardship withdrawals from 401k plans rise in warning sign of financial distress

| Option | Pros | Cons |

|---|---|---|

| Hardship Withdrawal | Quick access to funds | Taxes and penalties, depletes retirement savings |

| Loan | Provides funds without depleting retirement savings | Interest charges, risk of default |

| Credit Card | Convenient for short-term expenses | High interest charges, risk of overspending |

Financial Counseling and Support

If you’re struggling with debt or financial hardship, it’s important to seek help. There are many reputable organizations that provide financial counseling and support.

It’s alarming to see hardship withdrawals from 401k plans rising, a clear indicator of financial distress. This trend highlights the economic struggles many Americans are facing, and it’s a reminder that we need to prioritize financial stability. Meanwhile, the news of an appeals court ruling in favor of Trump amidst the New York fraud trial adds another layer of complexity to the already volatile political and economic landscape.

With so much uncertainty, it’s more important than ever for individuals to be proactive about their financial well-being and seek professional guidance when needed.

- National Foundation for Credit Counseling (NFCC):Offers free credit counseling and debt management services.

- Consumer Credit Counseling Service (CCCS):Provides credit counseling, debt management, and financial education services.

- Financial Counseling Association of America (FCAA):Connects individuals with certified financial counselors.

Preventing Financial Distress

Hardship withdrawals from your 401(k) are a sign of financial distress. While they may offer temporary relief, they come with significant downsides, including tax penalties and a reduction in your long-term retirement savings. It’s essential to take proactive steps to prevent financial distress and avoid the need for hardship withdrawals.

Building an Emergency Fund

An emergency fund is a crucial safety net that can help you weather unexpected financial storms. It provides a financial cushion to cover essential expenses during times of job loss, medical emergencies, or unexpected home repairs.

An emergency fund should ideally cover 3-6 months of essential living expenses.

- Determine Your Essential Expenses:Start by identifying your essential monthly expenses, such as rent or mortgage, utilities, groceries, transportation, and debt payments. Avoid including non-essential expenses like entertainment, dining out, or subscriptions.

- Set a Savings Goal:Multiply your essential monthly expenses by 3 to 6 to determine your emergency fund target. Aim for a minimum of 3 months of expenses, but strive for 6 months for greater financial security.

- Automate Savings:Set up automatic transfers from your checking account to your savings account on a regular basis, such as weekly or bi-weekly. This ensures consistent savings and prevents you from forgetting to contribute.

- Track Your Progress:Monitor your savings progress regularly to stay motivated and adjust your savings rate if needed. Celebrate milestones to reinforce your commitment.

Budgeting Effectively

Budgeting is a fundamental aspect of financial planning. A well-structured budget helps you track your income and expenses, identify areas for savings, and allocate your funds strategically.

- Track Your Income and Expenses:Use a budgeting app, spreadsheet, or notebook to record all your income sources and expenses for a few months. This will provide a comprehensive picture of your spending habits.

- Categorize Expenses:Classify your expenses into categories like housing, transportation, food, entertainment, and debt payments. This helps you identify areas where you might be overspending.

- Set Realistic Spending Limits:Allocate specific amounts for each expense category based on your priorities and financial goals. Adjust these limits as needed based on your financial situation.

- Stick to Your Budget:Regularly review your budget and track your progress. Make necessary adjustments to ensure you stay within your spending limits and avoid overspending.

Managing Debt Responsibly

High levels of debt can significantly impact your financial well-being and make it challenging to save for emergencies. Managing debt responsibly is crucial for long-term financial stability.

- Prioritize High-Interest Debt:Focus on paying down debt with the highest interest rates first, such as credit cards or payday loans. This minimizes the amount of interest you pay over time.

- Consolidate Debt:Consider consolidating multiple debts into a single loan with a lower interest rate. This can simplify your repayments and reduce overall interest costs.

- Negotiate Lower Interest Rates:Contact your creditors and request lower interest rates or more favorable repayment terms. Be prepared to negotiate and provide evidence of your good credit history.

- Avoid New Debt:Limit taking on new debt unless absolutely necessary. Focus on paying down existing debt and building your savings.

Benefits of Financial Planning

Financial planning is not just about saving money; it’s about achieving your financial goals and securing your future. Proactive financial planning can help you avoid financial distress and build a solid foundation for long-term financial security.

- Reduced Stress and Anxiety:Having a plan in place can reduce stress and anxiety related to finances, knowing that you’re prepared for unexpected events.

- Improved Financial Discipline:Financial planning promotes financial discipline, encouraging you to make responsible financial decisions and avoid impulsive spending.

- Increased Savings and Investments:By budgeting and planning for your financial goals, you can allocate funds effectively and prioritize savings and investments.

- Enhanced Financial Security:Financial planning helps you build a strong financial foundation, reducing the risk of financial distress and ensuring a more secure future.

Ending Remarks

While hardship withdrawals can provide a lifeline during a financial crisis, they are not a sustainable solution. It’s crucial to explore alternative options, such as accessing emergency savings, seeking financial assistance programs, or negotiating with creditors. Building a solid financial foundation through responsible budgeting, managing debt effectively, and establishing an emergency fund can help individuals navigate unforeseen challenges and avoid relying on hardship withdrawals.

By taking proactive steps to secure their financial future, individuals can safeguard their retirement savings and navigate the unpredictable path of life with greater confidence.