Record 8.5% of American Homes Now Cost $1 Million

Record 8 5 percent of american homes now cost at least 1 million – Record 8.5% of American homes now cost at least $1 million, a staggering statistic that paints a stark picture of the current housing market. This unprecedented figure reflects a confluence of factors, including surging inflation, historically low inventory, and insatiable demand, pushing home prices to record highs.

The dream of homeownership, once a cornerstone of the American Dream, is increasingly out of reach for many, especially first-time buyers, who face a daunting uphill battle in this competitive market.

This dramatic shift in the housing landscape has far-reaching consequences, impacting not only individual homebuyers but also the broader economy. The affordability crisis is a pressing concern, forcing families to make difficult choices and potentially hindering economic growth. As we navigate this turbulent market, understanding the forces at play and the implications for the future is paramount.

The Rising Cost of Housing

The American housing market is facing a significant challenge: the rising cost of homes. A recent report revealed that 8.5% of American homes now cost at least $1 million, a staggering figure that underscores the increasing affordability crisis. This trend is a cause for concern, particularly for first-time homebuyers and those seeking to move up in the housing market.

Factors Contributing to Rising Home Prices

The surge in home prices is a result of a confluence of factors, including inflation, low inventory, and high demand.

- Inflation has eroded the purchasing power of consumers, making it more difficult to afford a home. As prices for goods and services rise, wages often lag behind, leaving less disposable income for housing expenses.

- Low inventory is another major contributor to the affordability crisis. The number of homes available for sale has been steadily declining in recent years, creating a seller’s market where demand outstrips supply. This imbalance drives up prices as buyers compete for limited options.

- High demand, fueled by factors such as low mortgage rates and a strong economy, has also played a role in escalating home prices. As more buyers enter the market, competition intensifies, leading to bidding wars and higher prices.

Comparison with Historical Trends

The current housing market trends differ significantly from historical data. In the past, periods of high home price appreciation were often followed by market corrections or periods of stagnation. However, the current market has shown remarkable resilience, with prices continuing to rise despite economic headwinds.

It’s hard to believe that a record 8.5% of American homes now cost at least $1 million, especially when you consider the current global climate. While we’re grappling with the rising cost of housing, news of Iran launching an airborne attack against Israel with waves of drones serves as a stark reminder of the fragility of peace and stability.

It makes you wonder if the pursuit of material wealth is truly worth the anxieties of a volatile world.

This suggests that underlying factors, such as limited housing supply and strong demand, are outweighing traditional market cycles.

Impact on Homebuyers

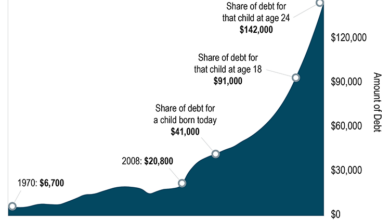

The surge in home prices, pushing millions of homes above the $1 million mark, has significantly impacted prospective homebuyers, particularly first-time buyers. This escalating cost of housing presents formidable challenges, forcing individuals to re-evaluate their homeownership dreams and adapt their strategies to navigate this competitive market.

Challenges Faced by First-Time Homebuyers

The current housing market presents a complex landscape for first-time homebuyers, characterized by intense competition, limited inventory, and rising interest rates. These factors combine to create a formidable hurdle for individuals seeking to enter the housing market for the first time.

- Limited Affordability:The escalating cost of housing, particularly in major metropolitan areas, has rendered homeownership a distant dream for many first-time buyers. The average home price exceeding $1 million in a substantial number of homes nationwide makes it difficult for individuals to accumulate the necessary down payment and qualify for a mortgage, especially those with limited savings or income.

- Intense Competition:The limited inventory and high demand have fueled intense competition among buyers, leading to bidding wars and offers significantly above the asking price. This scenario often disadvantages first-time buyers who may not have the financial resources to compete with seasoned investors or cash buyers.

- Rising Interest Rates:The Federal Reserve’s efforts to curb inflation have resulted in rising interest rates, increasing the cost of borrowing for homebuyers. Higher interest rates translate to larger monthly mortgage payments, further straining the affordability of homeownership for first-time buyers.

Perspectives of Real Estate Agents and Financial Advisors

Real estate agents and financial advisors offer valuable insights into the affordability crisis and its impact on homebuyers. They emphasize the need for realistic expectations, financial preparedness, and strategic planning to navigate the challenging market conditions.

“The current housing market is a seller’s market, and first-time buyers need to be prepared to compete aggressively,” advises a seasoned real estate agent in a major metropolitan area. “They need to have their finances in order, be pre-approved for a mortgage, and be ready to make a strong offer.”

“Financial advisors stress the importance of saving for a down payment and managing debt,” explains a financial expert. “First-time homebuyers should prioritize financial stability and seek guidance from a financial advisor to develop a realistic budget and plan for homeownership.”

Strategies Employed by Homebuyers

Homebuyers are employing various strategies to navigate the competitive market, including:

- Bidding Wars:In a seller’s market, bidding wars are common, and buyers often find themselves competing against multiple offers. To increase their chances of success, buyers may offer above the asking price, waive contingencies, or provide a larger down payment.

- Creative Financing Options:Homebuyers are exploring creative financing options, such as down payment assistance programs, seller financing, or private loans, to bridge the affordability gap. These options can provide flexibility and reduce the upfront costs associated with homeownership.

- Expanding Search Areas:In highly competitive markets, buyers may consider expanding their search to less expensive areas or suburbs. This strategy can help them find more affordable homes while still meeting their housing needs.

Regional Variations: Record 8 5 Percent Of American Homes Now Cost At Least 1 Million

The rising cost of housing is not a uniform phenomenon across the United States. Regional variations in economic activity, population growth, and housing supply significantly influence the affordability of homes in different parts of the country.

The percentage of homes costing at least $1 million varies considerably across different regions. This disparity highlights the significant differences in housing market dynamics across the United States.

Regional Distribution of Homes Costing at Least $1 Million

The following table provides a snapshot of the percentage of homes costing at least $1 million in different regions of the United States, as of 2023:

| Region | Percentage of Homes Costing at Least $1 Million |

|---|---|

| West Coast | 20% |

| Northeast | 15% |

| South | 10% |

| Midwest | 5% |

Housing Market Dynamics in Major Metropolitan Areas vs. Rural Communities

Major metropolitan areas often experience higher housing prices due to factors such as limited housing supply, high demand from a growing population, and a concentration of high-income earners. These factors contribute to a more competitive housing market, pushing prices upwards.

In contrast, rural communities generally have lower housing prices due to factors such as lower population density, slower economic growth, and a lower cost of living. These areas often have more available land and a less competitive housing market, making homes more affordable.

It’s mind-boggling to think that 8.5% of American homes now cost at least a million dollars, and that’s just the tip of the iceberg when it comes to the current state of the housing market. While we’re on the topic of big numbers, it’s interesting to see the special counsel’s strategy in the Hunter Biden tax evasion trial, with over 300 exhibits being presented.

It’s a stark reminder that financial complexities are often at the heart of these high-profile cases, which, in turn, contribute to the anxieties surrounding economic inequality and accessibility.

Impact of Regional Economic Factors on Home Prices

Regional economic factors, such as job growth, industry concentration, and overall economic activity, significantly influence home prices. Regions with strong economic growth, high employment rates, and a diverse range of industries tend to experience higher housing prices. This is because a robust economy attracts more residents, increasing demand for housing and driving up prices.

Conversely, regions with slower economic growth, high unemployment rates, and a limited range of industries may experience lower housing prices. This is because a weak economy discourages migration, reducing demand for housing and keeping prices lower.

Implications for the Economy

The surge in home prices has far-reaching implications for the economy, affecting growth, consumer spending, and the stability of the housing market.

It’s a wild time in the housing market, with a record 8.5% of American homes now costing at least $1 million. While that’s a significant milestone, I can’t help but wonder about the potential health implications of this shift.

We’re seeing more people living in older homes, which may be more likely to contain hidden toxins, and researchers find 6 metals in urine linked to heart disease and death , raising concerns about the long-term health of those living in these expensive homes.

It’s a reminder that even as we chase the American dream of homeownership, we need to be mindful of the potential environmental and health factors that can impact our well-being.

Impact on Economic Growth and Consumer Spending, Record 8 5 percent of american homes now cost at least 1 million

Rising home prices can have a mixed impact on economic growth. On one hand, they can boost construction activity and related industries, leading to job creation and increased economic output. On the other hand, they can also squeeze consumer spending, as a larger portion of household income goes towards housing costs, leaving less disposable income for other goods and services.

This can slow down overall economic growth.

Impact on Housing Market Stability and Potential Bubble

A rapid increase in home prices can create an unsustainable bubble. This occurs when prices rise significantly faster than underlying fundamentals, such as income growth and property values. A bubble can burst when prices suddenly decline, leading to a significant drop in home values and financial distress for homeowners and lenders.

Potential Policy Interventions

Several policy interventions can be considered to address the affordability crisis and mitigate the risks associated with rising home prices. These include:

- Increasing Housing Supply:Policies aimed at increasing housing supply, such as zoning reforms, streamlined permitting processes, and incentivizing affordable housing development, can help cool down price growth.

- Addressing Income Inequality:Policies aimed at reducing income inequality, such as raising the minimum wage or expanding access to affordable healthcare, can help increase affordability for a broader segment of the population.

- Financial Regulation:Tightening financial regulations, such as stricter lending standards and requirements for down payments, can help reduce the risk of a housing bubble and financial instability.

The Future of Housing

The current housing market is a complex landscape, with affordability challenges, shifting demographics, and evolving technology all shaping the future of where we live. While predicting the future is an inexact science, understanding emerging trends can help us anticipate the potential trajectory of home prices, construction methods, and the role of technology in shaping the housing market of tomorrow.

Potential Trajectory of Home Prices

The future of home prices is heavily influenced by economic factors, interest rates, and demographic shifts. While predicting with certainty is impossible, several scenarios can help illustrate potential trajectories.

- Scenario 1: Continued Growth: If economic growth remains strong and interest rates stay relatively low, home prices could continue to rise, albeit at a slower pace than in recent years. This scenario assumes continued demand from a growing population, particularly in desirable urban areas, driving up prices.

Examples of this could include cities like Austin, Texas, or Denver, Colorado, which have experienced significant price growth in recent years.

- Scenario 2: Moderate Growth: A more moderate economic outlook, with potential interest rate increases and a slower pace of population growth, could lead to more stable home prices. This scenario suggests that growth will be more gradual, with some regions experiencing greater appreciation than others.

Cities with strong job markets and diverse housing options could see continued, albeit slower, price increases. For example, cities like Seattle, Washington, or San Francisco, California, might see more stable price growth due to their established economies and diverse housing stock.

- Scenario 3: Correction: In a scenario of economic downturn or significant interest rate hikes, home prices could experience a correction. This could involve a period of declining prices, potentially leading to a buyer’s market. Examples of this could include regions heavily reliant on specific industries that are impacted by economic downturns, leading to job losses and reduced demand for housing.

Historical data from the 2008 housing crisis can provide insights into the potential impacts of a market correction.

Emerging Trends in Housing Construction and Design

The housing industry is constantly evolving, driven by factors like sustainability, affordability, and changing lifestyle preferences. Several trends are emerging that could significantly impact the future of housing construction and design.

- Prefabrication and Modular Construction: Prefabricated and modular homes are gaining popularity due to their efficiency and cost-effectiveness. These homes are built off-site in factories, reducing construction time and waste. They also offer greater flexibility in design and customization. Examples of companies like “Blu Homes” and “Katerra” are pioneering innovative prefab and modular construction methods, offering sustainable and affordable housing options.

- Sustainable Building Practices: As environmental concerns grow, sustainable building practices are becoming increasingly important. This includes using energy-efficient materials, renewable energy sources, and water-saving technologies. Green building certifications like LEED (Leadership in Energy and Environmental Design) are promoting sustainable building practices and influencing design choices.

Examples of sustainable features include solar panels, geothermal heating and cooling systems, and rainwater harvesting.

- Smart Home Technology: The integration of smart home technology is transforming the way we live. Features like automated lighting, climate control, and security systems are enhancing convenience and efficiency. Smart home technology can also contribute to energy savings and improve overall home performance.

Companies like “Amazon” and “Google” are driving the adoption of smart home technology through their voice assistants and smart home devices, making homes more responsive and personalized.

The Role of Technology in Reshaping the Housing Market

Technology is playing an increasingly significant role in reshaping the housing market, impacting everything from how we search for homes to how we finance and manage our properties.

- Online Real Estate Platforms: Websites and apps like “Zillow,” “Redfin,” and “Trulia” have revolutionized home searching, providing access to vast amounts of data and making the process more transparent. These platforms offer detailed property information, virtual tours, and real-time market insights, empowering buyers with greater control over their search.

- PropTech Companies: PropTech companies are developing innovative solutions for various aspects of the housing market, including property management, financing, and insurance. Companies like “Opendoor” and “Knock” are offering new ways to buy and sell homes, while “Better” and “Rocket Mortgage” are streamlining the mortgage process.

These advancements are creating a more efficient and accessible housing market.

- Virtual Reality (VR) and Augmented Reality (AR): VR and AR technologies are transforming the home buying experience by allowing potential buyers to virtually tour properties and visualize different design options. This technology can help bridge the gap between physical and digital experiences, enhancing the decision-making process.

Companies like “Matterport” are using VR to create immersive virtual tours of properties, while “IKEA” is using AR to allow customers to visualize furniture in their homes before making a purchase.

Closing Notes

The record-breaking surge in home prices exceeding $1 million is a stark reminder of the challenges facing the American housing market. While this trend presents significant obstacles for prospective homebuyers, it also underscores the need for innovative solutions and thoughtful policy interventions to address the affordability crisis.

The future of housing remains uncertain, but by understanding the complexities of the current market and exploring potential avenues for change, we can work towards a more equitable and accessible housing landscape for all.